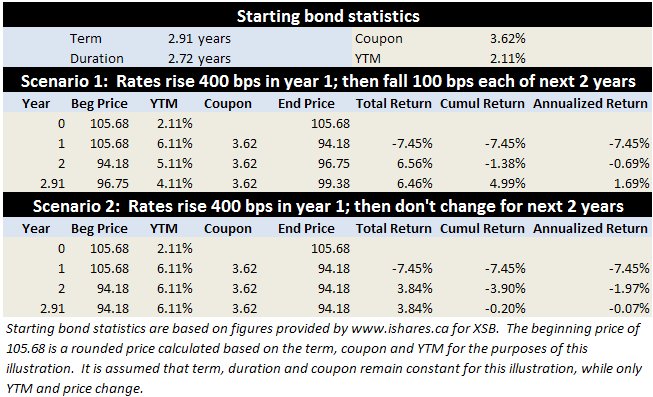

For those seeking a safe and dependable income source, today’s painfully low interest rates pose a real challenge. Bank of Canada Governor Mark Carney regularly reminds us that persistent low rates can be dangerous because they incent excessive borrowing. But low rates also pose some risk to the asset side of investors’ balance sheets. It looks like low rates will be here for a while so here are a few things to keep in mind when structuring investment portfolios.

Fees are critical

It has always been important to control the fees and expenses incurred to invest in bonds or bond investment funds. But as yields fall, fees increase in importance because they chew up a larger proportion of the starting yield. And this is an asset class with limited potential for outperformance by active managers.

Canadian bond mutual funds sport an average management expense ratio (MER) of 1.4% annually. The yield-to-maturity (YTM) of the Canadian investment grade bond market is an annualized 2.4 percent. Proportionately, that’s nearly 60% of bonds’ expected gross return. (Last fall, I explained some of the YTM’s finer points.)

Even five years is long enough to see fees’ powerful impact on net bond returns. For instance, the top performing bond funds over the past five years sport fees that are a fraction of the category average. That’s no mere coincidence but irrefutable math.

Don’t reach too far for yield

While the worst of the financial crisis may be behind us, the crisis isn’t gone. Recall that one of the crisis’ first signs in Canada was the asset backed commercial paper freeze in 2007. ABCP was held by many investors as a cash-substitute because it offered higher yields than safe treasury bills or other low risk short-term bonds. But we eventually found out that not only were these baskets of longer-term loans that were ‘rolled over’ or refinanced in the short-term but many also included higher-risk loans. In other words, reaching for yield was one of the sources of pain in the early days of the financial crisis.

Today, investors are becoming more enamoured with emerging markets bonds and preferred shares, both of which are valid portfolio components. But it’s important to establish limits on how much to put in riskier or less liquid securities offering higher yields.

REITs & dividend stocks are not bond replacements

While real estate investment trusts (REITs) and other dividend-paying stocks are often used to produce investment income, one must be cautious not to view these as bond replacements. The investment industry has been promoting stocks based largely on the juicy yields they offer today; often exceeding that available from safer bonds. But as I detailed in this December 13, 2010 blog post, there are good reasons to be careful of this reasoning.

Stocks are generally riskier than bonds so they should offer greater return potential. But the greater risk means that from time to time, investing in stocks will be a painful experience. By all means, look to high yield equities generally in the context of an income-oriented portfolio. But every portfolio needs at least some bond exposure to soften stock market volatility.

Beware of apparent ‘free lunches’

Investors and advisors are increasingly looking to so-called private placement funds that offer fat yields in this ultra-low-rate environment. One type, mortgage funds, make shorter-term loans to commercial property developers. There are more of these funds than I realized. One that I found claims to have earned 8% in each of the last nine calendar years. It further claims a 10% return in each of the four prior years – all interest. And the fund claims that the capital hasn’t risen or fallen – ever.

The fund is in a continuous offering, meaning that it’s open to new money. And it’s surprisingly liquid, allowing investors to buy and sell regularly. But think about this for a moment. These shorter-term loans are basically fixed income instruments – like bonds. And as interest rates fluctuate, these underlying loans’ market values should fall and rise accordingly.

As a base of comparison, short-term Canada bonds returned 5.1% in calendar 2011 but only about half was from pure yield. The rest came from capital appreciation from falling yields. But funds like these have unit prices that barely move, if they do at all – which punishes sellers in this scenario. So I’m a little skeptical of funds like this that neither rise nor fall in value to reflect changes in interest rates, credit spreads and liquidity.

All might be kosher with this and other similar funds but it’s naive to assume that any investment offering yields in the 8% to 10% range is not without material risk when short Canada bonds yield barely above 1% today.

Bond remain a critical portfolio component for virtually everybody. Keeping at least half of fixed income exposure in conventional investment-grade debt is a prudent policy. If you can’t resist reaching out for more yield, keep these tips in mind to help avoid making poor decisions with what should be a portfolio’s conservative foundation.