The relevance of YTM & the impact of rising rates

By Dan Hallett, CFA, CFP on July 7th, 2011

Last week, I wrote about not reading too much into distributions paid by bond mutual fund and bond exchange-traded funds. I admit to being surprised by the sensitive chord this struck with many investors. In the spirit of brevity and focus, I glossed over some finer details pertaining to bond yields. So, this week, I delve a bit deeper into a few issues that emerged from the many public and private messages I have received over the past week.

Clarifying YTM

The main thrust of last week’s post was to prompt investors to focus more on YTM than on current yield or distribution rates. But even YTM is a theoretical figure.

Technically, a bond’s YTM is the rate of return that equates the purchase price of a bond with the present value of all future coupon payments and the repayment of the maturity (or par) value. I gave the impression that a bond’s YTM is a definitive measure of a bond’s future return when held to maturity. While it’s the best forward-looking estimate available, it’s not precise.

The YTM formula assumes that all interest payments are fully reinvested (without cost) into the same bond at the YTM. This just isn’t possible because yields and YTM levels aren’t constant; and full reinvestment at no cost isn’t possible.

Relevance of YTM

Many sharp readers pointed out that most bond funds and ETFs don’t just hold bond to maturity, which would make the YTM figure less relevant. This is a good point. In fact, I was surprised by the amount of turnover in what is supposed to be a ‘passive’ bond fund. Yet the iShares CDN Short-Term Bond Index ETF (XSB) has turned over its portfolio more than 60% annually over the past five years. (See page 9 of XSB’s 2010 Management Report on Fund Performance for year-by-year turnover data.)

Despite the above points on the imprecision of YTM and the fact that bond yields can and do change, an investor’s ultimate return can’t be known with certainty in advance at any point in time. But the YTM remains an excellent indicator of future total return over the term of the bond (or average term of a bond fund). To that point, I would urge investors in bonds and bond funds/ETFs to focus on YTM when looking at return potential at the time of purchase.

Impact of rising rates

Many are leery of bonds today because of the prospect of rising interest rates (and the downward price pressure that would result). And some argue that YTM isn’t such a good indicator of future fund or ETF return in a rising rate environment. In this context, there are two important noteworthy points.

First, in all of my seventeen years in this industry there has been a near-constant sentiment that historically-low interest rates are poised to rise. It’s true that the farther rates fall, the less room they have to fall. However, as I wrote last year bonds remain one of the key portfolio building blocks. While some might de-emphasize bonds a bit based on an expectation of rising rates, you don’t want to be out of them altogether.

Second, while many have been calling for the end of the bond bull market and the damage that awaits bond-heavy investors, I have rarely seen any quantification of the potential losses that bond investors could suffer. So, I ran some simple calculations.

Bond bear market scenarios

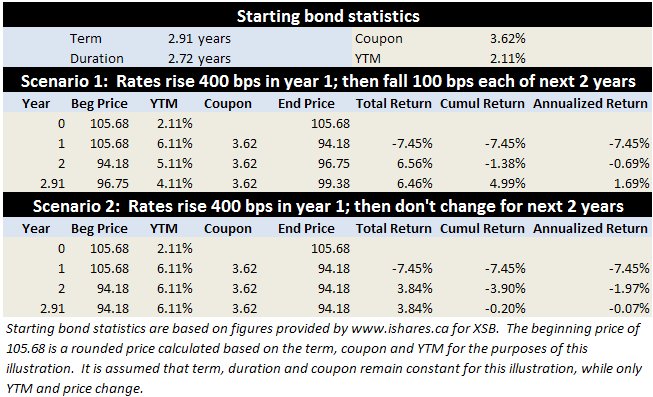

Since XSB is the focus of last week’s post and the topic of many other articles, I start this illustration with a bond portfolio with a YTM of 2.11%, an average coupon of 3.62%, a term of 2.91 years and a duration of 2.72 years (all stats from the XSB profile page as of June 30, 2011). Let’s assume that rates shoot up by 400 basis points in year one, kind of like they did in 1994.

Even 1994, the worst bond market since 1981, was followed by what turned out to be one of the best years on record for bonds. In other words, bond yields don’t usually shoot up sharply and stay there. They fluctuate. So, if that initial 400 basis point rise is followed by two years of falling rates – e.g. each year falling by 100 basis points – the total return would be around 5% over the 2.91 year holding period. That’s a loss of 7.45% in year one, followed by two years of about 6.5% gains, as shown in the table below. That’s not bad considering the steep loss in year one.

What about the fear of rates rising and staying there? The second scenario assumes the same 400 basis point rise in bond yield in year one. But instead of subsequently rates falling, I assume that they stay flat after year one. The result for year one is the same – i.e. a 7.45% loss. With no rate changes, prices would remain stable thereafter. But coupon interest would continue to be paid. So, if you hold XSB for a time period equal to its average term to maturity – 2.91 years as of June 30 – you’ll basically be flat (technically a loss of 0.2% over the 2.91 years). So even in a very negative scenario, capital remains largely intact over the average term of the fund. The table below summarizes these two scenarios, showing selected data.

Even though the bonds in an ETF aren’t left to mature and assuming a fairly bearish scenario, simply holding a bond fund or ETF for a time period equal to its term upon purchase should minimize the chances of loss. And if yields bounce around in both directions, as has been the case in the past, the chances of losing money are even slimmer. Applying a similar analysis to mid-to-long-term bond funds would show similar results.

As I was finishing this post, I found two other related articles. Read John Heinzl’s answers to reader questions about bonds vs. bond ETFs in the Globe and Mail. Also, blogger Canadian Couch Potato does an excellent job of exploring the prospect of rising rates and how that might impact different parts of the bond market.