Want to scratch your market timing itch? Try some disciplined rebalancing

By Dan Hallett, CFA, CFP on February 15th, 2013

Many investors feel better about their investments when their advisor is fine-tuning their portfolios. The persistence of global macroeconomic challenges has strengthened this long-standing desire among many clients. While so few are skilled market-timers, perhaps a sensible and disciplined rebalancing method can scratch that market timing itch while controlling risk.

Many mutual funds set out to market time or shift money tactically. Many produced head-turning returns for a few years only to see – with very few exceptions – their long-term records sink into mediocrity. Given that portfolio managers can’t do this well, it’s unrealistic to expect financial planners and advisors to even attempt this tall feat. That’s where rebalancing comes in.

Purpose of rebalancing

Fluctuating market prices will push holdings above or below their original allocations. Rebalancing involves simply trimming your winners and using the proceeds to add to underperformers.

Without a well-defined process, most investors and advisors have a tough time pulling that rebalancing trigger. It’s no wonder. Price momentum, well-documented in academia, has persisted in financial markets around the globe for decades. Rebalancing too frequently can prevent portfolios from capturing some of the benefits of momentum.

But letting stocks, for instance, run too far up may push investors into an uncomfortable level of risk. So a good rebalancing method must balance the desire to capture the momentum effect while controlling risk.

After considerable discussion and research a few years ago, our firm settled on a +/- 20% method whereby we invest clients at target allocations, and allow their allocations to each chosen manager to drift up or down by 20% of the target. Whether this hurts or boosts returns depends on the time frame studied and the markets’ return patterns.

Our research shows that this method would have produced the expected result of capturing momentum while limiting risk. This is supported by a January 2008 Journal of Financial Planning article by Gobind Daryanani (Opportunistic Rebalancing: A New Paradigm for Wealth Managers).

Interestingly, this rebalancing method has also triggered well-timed shifts which is why I think it could fill the role of occasional market timing tool.

The results so far

I constructed a hypothetical portfolio made up of indices tracking Canadian stocks (20%), global stocks (40%) and Canadian bonds (40%). I set rebalancing thresholds at 20% on either side of each index. For instance, Canadian stocks would be rebalanced if they sink below 16% (0.8 x 20%) or rise above 24% (1.2 x 20%) of this portfolio.

And whenever any one of the three components breaches its allowable range, all holdings are rebalanced back to their initial targets – which happened 13 times in 33 years. I used monthly data from 1980 through 2012 – i.e. allocations are evaluated monthly to see if they remain in the allowable ranges or if rebalancing is necessary.

The table below (click on it to enlarge it) summarizes this portfolio’s risk and return profile using three rebalancing methods: no rebalancing, our +/- 20% method and monthly rebalancing. It’s worth repeating that in trending markets – as in calendar 2012 – no rebalancing at all will be the top performing strategy. Choppy markets will be kindest to frequently-rebalanced portfolios.

Prior to back-testing different methods, we expected that a more balanced set of rules would capture sufficient momentum without materially increasing risk – which was the case in the past.

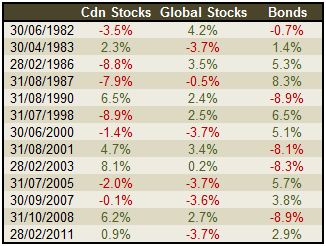

As we looked more closely at our chosen rebalancing method, we noticed that it often called for a portfolio rebalance near market extremes. The table below shows the asset mix shifts that would have resulted over the past 33 years if following our +/- 20% rebalancing method described above.

Notice the rebalance out of stocks and into bonds just two months before the big crash of 1987. In the summer of 1990, again at a low point for stocks, following this method would have prompted an addition to stocks and out of bonds. There were some misses to be sure but overall, this method worked and it has resulted in a bunch of value-added shifts since 2000.

I don’t want to over-sell this. The statistics are not robust enough to assign any real significance to this rebalancing method as a great market timing tool – though I’d say it’s as good as any.

But when you overlay sensible portfolio risk controls, you can keep portfolio risk in check (the main purpose) while often making well-timed asset mix shifts. And that might be just enough to scratch that itch – that is if you can follow it.