Volatility measures behavioural risk

By Dan Hallett, CFA, CFP on October 18th, 2010

In his latest Globe & Mail column, Tom Bradley discussed risk and volatility. Modern finance theory uses volatility, or more formally standard deviation, as its measure of risk largely because it is an easy statistic to use in quantitative modeling. Volatility measures how far an investment’s returns move away (or deviate) from its average based on its daily, weekly or monthly returns.

Since volatility does not differentiate between movements above or below an average, many disregard the popular measurement as a poor risk measurement. I shared that opinion for the first several years of my career. I reasoned, quite logically, that volatility doesn’t matter if it’s on the upside and that the impact of the swings in value would diminish as the holding period lengthens. The problem is that few investors possess the discipline and logical mindset when it counts most – a conclusion I reached a decade ago.

Tom writes, in part:

A high-potential, high-volatility portfolio should generate better returns over time, but it has to match up with the investor’s psychology. As investment professionals, we run the risk of doing what trainers at the gym do. Too often they develop textbook programs with all the required exercises, but fail to take into account their clients’ time, willpower and exercise history. Routines that are shorter, less perfect and more fun would have more staying power and get better results.

In the investment context, Dan Hallett of Highview Financial Group has done research that suggests investors in less volatile balanced funds have a longer holding period and achieve better returns than those in all-equity portfolios.

Not only do balanced fund investors do better than stock fund investors, but they also do better than investors holding a balanced mix of separate stock and bond funds.

In a recent blog post, I wrote about how ironic it is that generally pricey balanced funds induce better investor behaviour compared to investing in stocks and bonds via separate funds. Despite balanced funds’ higher fees, balanced fund investors make more money. In other words, the behavioural benefits of balanced funds more than offset the fee premium that most balanced funds charge. Two charts from our past research illustrate this.

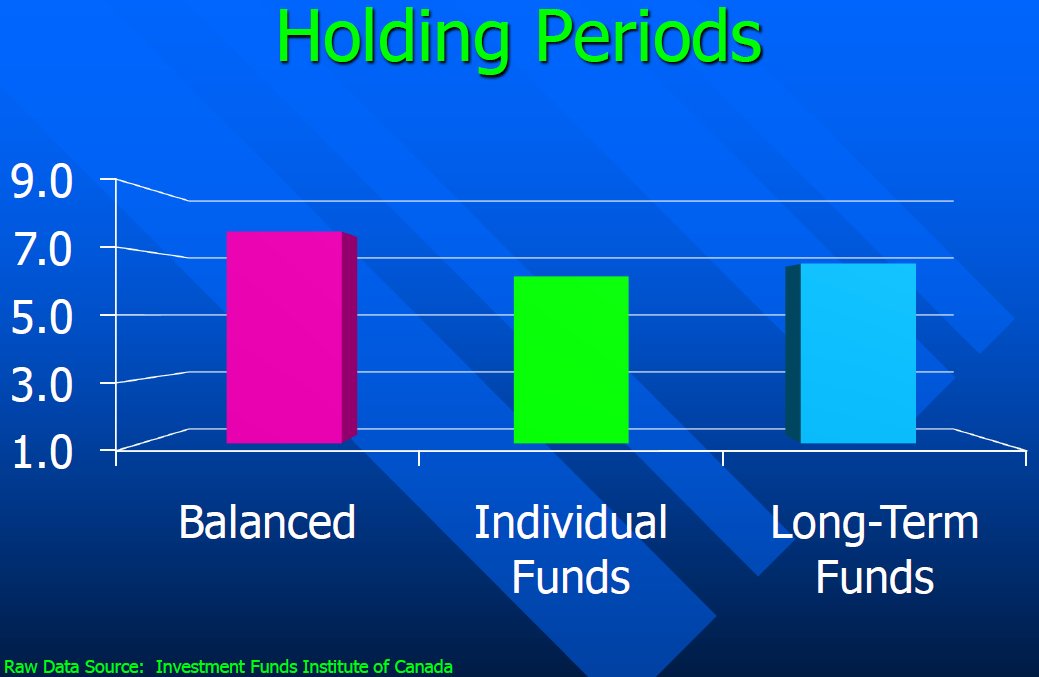

The chart below, taken from my presentation at the 2007 Morningstar Investment Conference, shows my calculation of dollar-weighted holding periods for various types of mutual funds. From late 1993 through the spring of 2007, balanced fund investors held their funds for a median period of 7.6 years. I estimate that investors buying a balanced mix of separate stock and bond funds held their funds for a median of 6.2 years. As a base of comparison, investors in all non-money-market funds held onto their funds for a median of 6.6 years.

I have long believed that longer holding periods lead to better returns – a conclusion reached by Brad Barber and Terrance Odean in their extensive analysis of brokerage accounts. The research of ours that Tom Bradley referenced supports this notion.

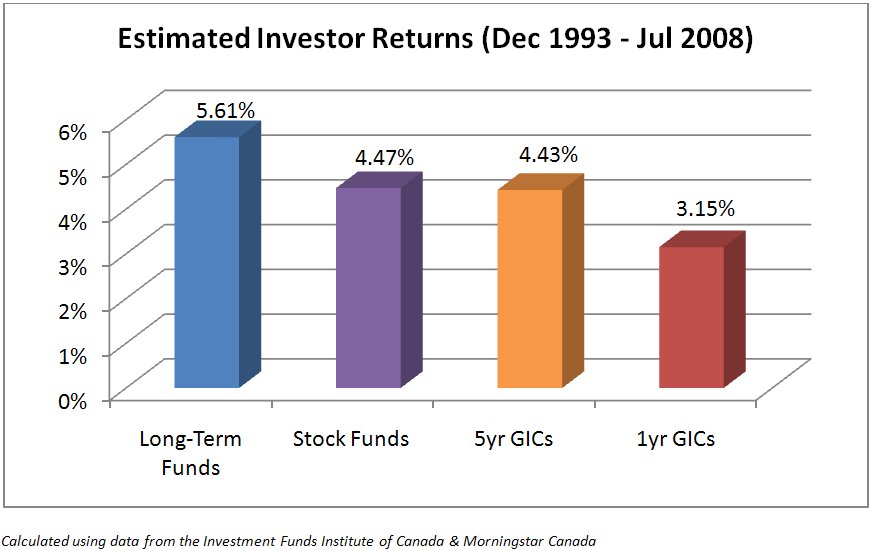

The chart below shows that even before the worst of the bear market, stock fund investors didn’t really enjoy any of the extra return available from (and expected when) investing in stocks – even over a fifteen year period. The below chart represents aggregate data but it’s consistent with individual fund comparisons I’ve done over the years.

Critics of the investment industry will point to fees as a big culprit. And they have a point. But just like the balanced fund illustration above, the impact of investor behaviour dwarfs the importance of fees. So I was wrong to dismiss standard deviation as a risk measure for all of those years. It’s not a measure of investment risk but a measure of behavioural risk. Still, standard deviation measures a type of risk that has potentially damaging consequences.

We used mutual funds for our research because the data is readily available. But the same research applies to most other investment vehicles and portfolios. Whatever your investment vehicle of choice, don’t dismiss volatility as a risk measure. But understand just what kind of risk it measures.