Should you hold bonds in taxable accounts?

By Dan Hallett, CFA, CFP on January 6th, 2012

An investor’s asset allocation strategy refers to how money is divided across different classes of investments – i.e. stocks, bonds and cash. An asset location strategy, however, drills down a level deeper and deals with “where” or in which accounts to hold your chosen stocks, bonds and cash. Today’s bond yields might prompt some investors to challenge conventional asset location advice.

Traditional Asset Location

Investors fortunate enough to have money to save and invest over and above their RRSP and TFSA contributions need both asset allocation and asset location strategies. The standard advice is to stuff all of the bonds in RRSP, TFSA and similar accounts to defer or shelter tax on interest income (otherwise 100% taxable). Similarly, stocks usually dominate non-registered accounts because they generate more lightly-taxed capital gains and (in the case of Canadian stocks) dividends.

But with bond yields having fallen (i.e. bond prices having risen) in the face of weak stock prices, this traditional asset location advice may not hold for everyone.

Minimize Expected Taxes Payable

Efficient asset location decisions are driven by minimizing taxes payable on investments. But actual taxes can only be confirmed after the fact. Accordingly, we need to make several assumptions to estimate future taxes from investment activities.

Assuming stocks return 8% annually and bonds post returns of 2.36% per year (Canadian bonds’ yield to maturity at the time of writing), bonds might be best held outside of registered plans like RRSPs and TFSAs for higher-income investors. Alternately, those with a five-figure taxable income may want to stick with conventional asset location strategies.

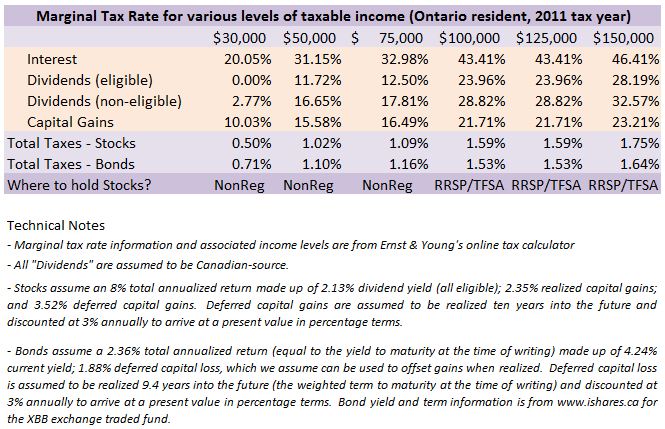

The reason is simply that higher total returns usually result in higher taxes (particularly for higher income individuals). And with bonds sporting razor-thin yields, they don’t stand to generate a heavy tax burden because the pre-tax return potential is so low. In other words, even though the tax rate applied to stock investing is lower compared to bonds, stocks’ higher expected return may result in a higher dollar amount of tax for some. The table below (click to enlarge it) summarizes some calculations and the many assumptions made for this illustration.

Stop, think and assess

Despite the apparent precision, I can’t stress enough that the above table is a very general illustration. For any given situation, the conclusion can swing either way.

For instance, if stocks produce a still-respectable but lower 7% annualized return (or much lower), it will probably make more sense to hold stocks in non-registered accounts. But investors buying only high-yield stocks – a popular strategy today – may save taxes by doing the opposite and keeping that yield in registered plans to defer or shelter the tax.

Investors need to stop, think and assess before blindly following traditional asset location advice. In a general context, the conventional wisdom remains sound. But with low bond yields, it’s worth running through some scenarios to help in this decision. And if you end up holding your bonds outside of registered plans, you might consider one of more tax-friendly bond alternatives available. In what may be a lower-return environment, any return enhancement is worth considering.