It is time to prepare for the bear

By Dan Hallett, CFA, CFP on November 26th, 2014

All year I’ve been wanting to write an article urging advisors and individual investors to prepare for the next bear market. When stock markets hit a pothole in late summer and early fall, it struck me as an opportune time to refresh this idea. While markets have since quickly moved past the decline, I was struck at the amount of attention given to what I thought were normal stock market fluctuations.

The decline from early September through mid-October was more significant for Canadian stocks than for other major stock markets. Below is a table showing returns of a selected list of markets and asset classes during this recent period.

Canadian small company stocks, commodity stocks and some smaller foreign country stocks were hit pretty hard but none were in bear market territory. Moreover, bonds were up by about 1% – making for a very modest decline for balanced portfolios during this stretch.

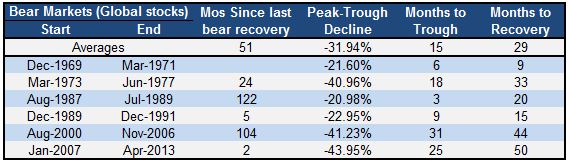

While too much attention was paid to declines during the above-referenced period, the fact that many people worried about such a routine fall in value is a useful reference point to starting the bear market discussion. I devoted my column for Investment Executive’s mid-November issue to the idea that advisors should start preparing clients for the next bear market. I cite a number of bear market summary statistics in the article. There was no room for tables so below are bear market summaries for U.S., Canadian and global stocks.

What I didn’t cover in my IE column was how specifically to speak to this issue with clients. The above tables can help to illustrate the history of bear markets – particularly the U.S. table since that’s the market for which I have the most data. The conversation need not be complicated.

I was in a client review meeting recently. Performance clocked in at about 8% (net of fees) for this client’s first year. This client’s target – i.e. the return needed to achieve his goal – is about 4.5%. I explained that our initial expectation was for his portfolio to hit this target net of all costs compounded over a long period of time. In year one we achieved 8% – well above his target – but that we still expected the combination of this strong first year and future returns to average out to about his target return.

The average can fall from the current 8% either via a string of many lower-return years or – more likely through the occurrence of another bear market. I didn’t have these tables handy but I pointed out that bear markets have always happened and they likely always will. So another is coming at some point – I don’t know when – but when it occurs, our disciplined rebalancing will kick in at a relatively low point and trigger a shift out of bonds and cash and into stocks.

I warned him that it will be uncomfortable when a rebalance is taking place but that it will ultimately position the portfolio to recover more quickly and help increase the odds of achieving his goals. And in the meantime, we always ‘carve out’ a cash cushion to fund any shorter-term cash needs.

This client’s bear market education will continue through future communications and meetings. And of course, when the next bear market materializes this client will be as well prepared as possible.