Investors Need More Meaningful Risk Measures

By Dan Hallett, CFA, CFP on July 22nd, 2015

The measurement and communication of risk for investment funds is high on securities regulators’ radar. They continue to review this important issue and we’re awaiting their final decision. It’s striking how many years have passed, yet the industry continues to debate many of the same issues.

The measurement and communication of risk for investment funds is high on securities regulators’ radar. They continue to review this important issue and we’re awaiting their final decision. It’s striking how many years have passed, yet the industry continues to debate many of the same issues.

In 1997, I started working for a firm that was trying to move the industry away from opaque academic risk measures like standard deviation to more common-sense methods. I have written several times that the industry standards for risk measure and illustration are inadequate and meaningless. The announced changes in fund risk ratings offer plenty of new evidence to support my argument.

Risk Ratings

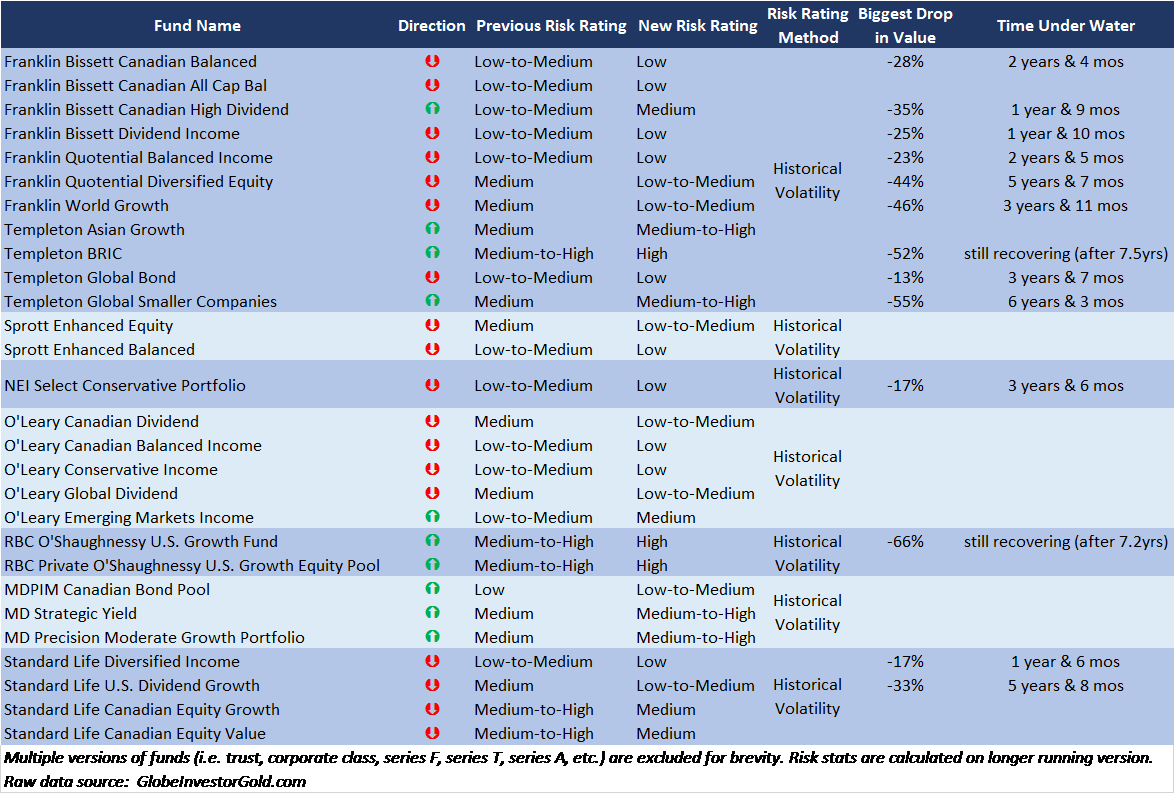

I tracked risk rating changes on 44 mutual funds since last October. The table below lists the affected 28 unique funds – excluding 16 funds that are simply other incarnations of the 28 – and summarizes the risk rating changes and related risk statistics.

Nearly two thirds of the affected funds saw falling risk ratings with just over one third seeing a bump up in risk rating. In my view, an investor’s exposure to risk should not fall after a multi-year run up in prices. A case can be made for risk being higher since we are likely closer than not to the next significant price drop.

But since the industry remains stuck on measuring risk using standard deviation – and applied to arbitrary scales – fund sponsors are blindly lowering risk ratings in droves. And risk ratings will only rise under this system after the worst of the next decline has already occurred – i.e. when it’s too late.

Volatility in the Markets

Those using the industry standard risk rating method will update volatility measures annually. If volatility has fallen sufficiently over the past three or five years, there’s a good chance the risk rating will fall. The thing is that usually volatility falls during bull markets and rises during bear markets. By the time this is captured by fund companies’ annual updates, investors will have already been hurt. Even worse, when bear markets fall out of the three and five years periods used to assess risk, standard deviations are bound to fall.

A system designed to truly inform and protect investors would look far back enough to capture bear market performance either for the fund or – if it’s too new – for its benchmark. Combining this with a more common sense measure – i.e. how much a fund lost in its last big decline – puts these new risk ratings in a different light.

Of the 28 funds in the above table, 13 have enough history to look at past bear markets. Six of these 13 funds sport a new “low” risk rating. These six so-called “low risk” funds lost an average of more than 20% in the last bear market and spent 2.5 years under water. I don’t know anyone who considers this low risk.

The few other funds that were re-assessed as having “low to medium” risk sport an average bear market loss of more than 41% and spent more than 5 years climbing back to the previous high.

If the industry continues to argue – as most fund companies have – that the standard risk rating method works well, they will need to rethink the purpose of these ratings. All fund companies are legal fiduciaries. Yet a true fiduciary mindset would attempt to measure and illustrate risk in ways that better inform investors.

In my submission on this topic to Canadian Securities Administrators last year, I clearly outlined the weaknesses of the status quo and provided strong arguments for with examples of more meaningful solutions (e.g. see page 4 of my submission). The latter reflects what we show to clients both before they engage our services and through our periodic reporting. It’s time for the broader fund industry to abandon its opaque technical approach and become more investor-friendly so that its end clients can better grasp risk before they invest.

>> HighView Financial Group is an investment counselling firm for affluent families and foundations. We build portfolios based on each client’s unique goals and tolerance for risk. Schedule a complimentary discovery session to see if we’re the right investment stewardship counsellors for you.

You may also be interested in:

- Illiquidity may be floating rate funds’ biggest risk (July 30, 2014)

- Fund risk rating change highlights need for reform (April 4, 2014)

- Industry risk rating failing investors of floating rate note funds (September 17, 2013)

- Fund Facts a good start but risk rating & suitability get thumbs down (July 13, 2011)

- Fund Facts won’t enlighten investors (November 2007)