Illiquidity may be floating rate funds’ biggest risk

By Dan Hallett, CFA, CFP on July 30th, 2014

Floating Rate Debt (FRD) is getting an increasing amount of attention. Over the past year, several new products have been launched focusing on floating rate debt such as leveraged loans and so-called senior loans. All pay floating rates of interest – a feature that is too heavily promoted for my liking – while offering juicy yields to entice investors. The marketing of such funds is misleading in my view.

The industry boasts loudly about how such funds can protect investors from rising yields. While there is little mention of downside risk potential, at least most are up front about the credit risk profile of floating rate and senior loan funds. But funds with large holdings in bank loans face a potential liquidity risk that usually gets nothing more than a passing mention – if anything at all. And that’s a practice that needs to change before the next credit market meltdown.

Settlement Terms: bonds vs. loans

Key to understanding the liquidity risk is understanding the differences in how loans are traded and how that differs from bonds (i.e. securitized debt instruments or fixed income securities). Settlement terms refer to how long before buyers must pay for their purchased investments and when sellers are entitled to proceeds from the investments they’re selling. Stocks and bonds settle on T+3 settlement terms. For instance, if you sell a bond on Monday, the proceeds are added to your cash by Thursday (i.e. three business days after the date the trade is filled).

Bank loans can settle as quickly as T+5 or as long as T+40 according to page 4 of this BlackRock presentation on floating rate notes and bank loans. To put that into perspective, 5 business days equates to a full calendar week (assuming no holidays). Forty business days is about two months on the calendar.

Bonds, debentures and notes settle on T+3 terms – the same terms applicable to mutual funds, ETFs and other exchange-traded securities. But according to a recent Bloomberg article, bank loan trading requires the involvement of lawyers and clerks to review and vet documents for every trade. The liquidity risk stems from a mismatch of placing these relatively illiquid loans inside of a legal structure that is very liquid.

In the extreme cases of direct property, labour sponsored funds and other illiquid investments investors could end up making an unintended lifetime commitment.

(Mis)truth in labelling

Holdings labels are vastly different between website profiles, Fund Facts disclosure documents and financial statements. In some cases fund holdings are lumped into rather generic “corporate debt” label. Sometimes moving to Fund Facts provides more detail in terms of how much is held in term loans and how much is in more liquid bonds. At other times, only published financials have proper holdings classifications. And this needs to be improved. Take Trimark Floating Rate Income, one of the oldest funds, for example.

Its website shows a geographic breakdown only. The top holdings list indicates that this fund may hold a bunch of loans – not more liquid bonds. The fund’s monthly profile and Fund Facts document each shows a big allocation to “floating rate debt” but neither breaks out how much is in bonds vs. loans. It’s not until I pop open the financial statements that I see a real breakdown of bonds vs. loans. I feel for the individual investor because this is representative of this group of funds – not an isolated case. What’s striking is how clear and easy the same firm makes this exercise for its TSX-traded Senior Loan ETF.

I should highlight the O’Leary Floating Rate Fund’s prospectus for being better than most in speaking to liquidity risk; specifying that its holdings could see settlement terms as long as T+19 when buying or selling loans. I have in the past directed well-deserved and sharp criticism at the firm (e.g., for its aggressive marketing, for talking up its book, etc.). But on this issue they deserve kudos.

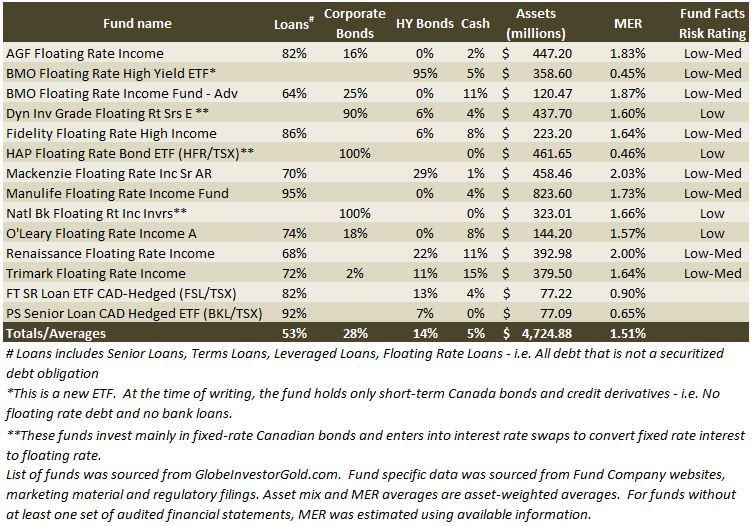

Floating rate fund asset mix

In the table below (click to enlarge it) I’ve attempted to present a clearer picture of how much each floating rate or loan fund holds in bonds and bank loans. A few funds boast low credit risks and good liquidity. The other ten funds are stuffed with less liquid bank loans. I hope that the below table will help those who are so focused on protecting against rising rates become more aware of the liquidity risks they’re assuming in exchange.

See also…

Industry risk rating failing investors of floating rate funds (The Wealth Steward)

Fixed Income’s new reality (Tom Bradley, Steadyhand Investments)