Desperately seeking income

By Dan Hallett, CFA, CFP on June 21st, 2012

The Globe and Mail recently reported that Michael Lee-Chin was planning a return to the retail investment industry. He has spoken specifically about his desire to bring institutional private equity exposure to retail investors in Canada. It’s a good idea on the surface but a look into similar past efforts might make investors and their advisors a bit cynical pending further details. Bringing institutional ideas to the retail market is a well-worn path peppered with pot-holes.

Real Estate

Canadian pension funds are effectively some of the largest landlords in the country. Ontario Teachers’ Pension Plan has owned Cadillac Fairview since the mid-1990s. OMERS acquired Oxford Properties in 2001. La Caisse de dépôt et placement du Québec owns Otéra Capital, a big commercial lender. And there is talk that pension plans are now eyeing real estate investment trusts (REITs) as potential acquisitions. Pension plans are hungry for commercial real estate’s cash flow generation potential and embedded inflation protection to meet their plans’ future spending liabilities.

Retail investors could once access funds with direct property holdings but they’ve hit major liquidity squeezes at least twice over the past two decades. There is no easier way to scare away investors than to tell them they can’t access their money when they want it most. That’s what direct-property real estate funds did in the early 1990s (and again during the recent financial crisis).

But just a few years later, real estate mutual funds had a renaissance. Dynamic and CIBC launched real estate funds in 1996 and 1997, respectively. Many others eventually followed (despite falling out of favour in 1998-2000). These newer funds – which invest in shares of real estate companies and REITs – have two snags.

Fess are generally high. And with a focus on public market securities there is a lot of stock market ‘noise’ built into the short- and intermediate- term price activity of public securities. So investors either had to sacrifice liquidity for direct property exposure or be one level removed from that exposure to obtain their desired liquidity at the expense of diversification. But both types of funds sport high fees.

Infrastructure

The story is similar, though younger, with infrastructure funds. It was the better part of a decade ago when pension funds began snapping up stakes in toll roads and bridges – which gave birth to the infrastructure theme. The motivations were identical to real estate – indexed cash flow potential – and the story almost sold itself as investors were licking their post-2000 bear market wounds.

But when infrastructure mutual funds began to appear about five years ago, I was struck by the high fees (which still average about 2.7% annually). Two additional wrinkles had to do with exposure and definitions.

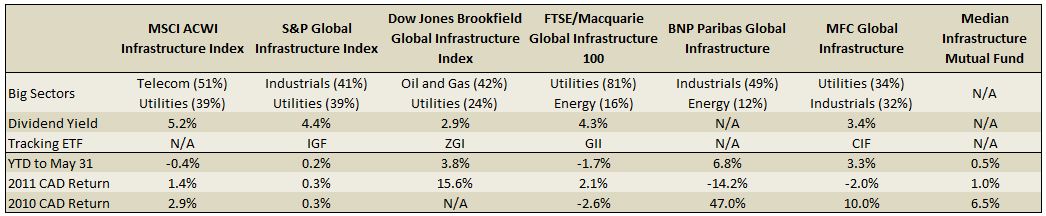

As with real estate funds, infrastructure mutual funds don’t directly invested in the actual infrastructure assets but rather in more liquid shares of companies that manage or service such assets. And while there are a handful of infrastructure indices, the providers seemingly have varying definitions.

The range of holdings, dividend yields and returns shown in the table below signal a wide range of content across the different index providers and, in turn, by the many funds pursuing this popular theme. (Click on the table below to enlarge.)

Sources: MSCI, S&P, iShares, State Street, Dow Jones, FTSE/Macquarie, BNP Paribas, BMO, MFC

Many retail investors – and their advisors – are desperately seeking higher-income solutions in this ultra-low-rate environment. And institutional investment themes continually draw the retail sector to the trough – but usually only after the easy money has been made. Unlike institutions, however, retail investors must accept trade-offs. In an ideal world, retail exposure to institutional investment themes would boast abundant liquidity and reasonable fees to go along with their high income. But this has proven to be an elusive combination as high fees have squeezed returns and exposure is sacrificed for liquidity.

It’s always possible that future product offerings will prompt the declaration “this time is different”. I’m doubtful but would be happy to be proven wrong.

—————————————–

See also: The unintended lifetime commitment (March 2012)