Covered-call funds haven’t delivered the goods

By Dan Hallett, CFA, CFP on September 7th, 2012

Covered-call writing is an investment strategy that promises significantly lower risk with little or no give-up in return potential. But I argued in a recent post that the odds were fundamentally against investors realizing this potential since I expected the risk reduction to be insufficient to make up for the forgone upside. And a look at real life portfolios executing this strategy supports this view. My admittedly limited study so far suggests that stock selection, transaction costs and forgone upside have proven to be formidable performance hurdles.

There isn’t an easy way to filter for funds using covered call strategies. Those in Canada are either very new – like the funds from First Asset, BMO and Horizons – or have mixed strategies. And some of the older covered call closed-end funds I found either have a capital repayment feature or have a very mixed history muddied with fund mergers and mandate changes. So my analysis began with an older but unique Canadian example.

Same firm, different mandates

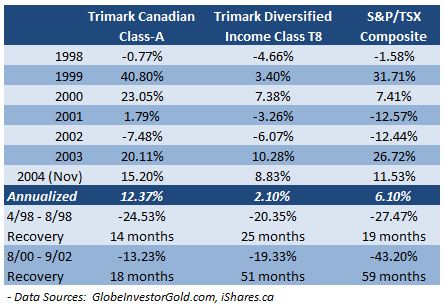

GT Global was a small fund company that is now part of Invesco Canada. This Canadian subsidiary of a European firm had two Canadian stock funds – often run by the same manager – that both invested in Canadian stocks with one important difference. One fund used a covered call strategy to generate income and other did not. The funds still exist today as Trimark Canadian Class (the option-free fund) and Trimark Diversified Income Class (the covered-call fund). While the funds are very different today and neither employs covered-calls, their older returns offer a useful comparison.

The funds underwent significant changes in late 2004 so the table below compares performance of the two funds from calendar 1998 through November 2004 – along with some bear market statistics. S&P/TSX Composite Index returns are included for context.

During much of this period, the two funds shared lead managers. Notice that while the covered call fund generally lost less in bear markets, its capped upside in bull markets stunted the covered-call fund’s recovery potential – despite milder losses.

The huge under-performance of the covered call fund was also partly due to the fact that the unrestricted fund was able to buy smaller cap deep value stocks that weren’t option-eligible but that were dirt cheap (and outperformed in the second half of the above time frame). The covered call fund, however, needed to focus on stocks with sufficiently-liquid options available to execute its strategy.

So in this case, stock selection was a key driver behind the performance gap. Advocates of this strategy might point to Canada’s narrow options market and to the U.S. as a much better market in which to implement this strategy. But the data I’ve examined doesn’t support this notion.

The U.S. experience

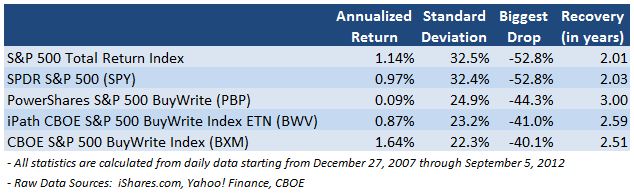

Searching for ETFs, I found only two funds that have some history of employing this now-popular strategy – PowerShares S&P 500 BuyWrite (PBP) which started in late 2007 and the iPath CBOE S&P 500 BuyWrite exchange traded note (BWV) which began in the spring of 2007. The table below shows performance statistics for these two products, a plain vanilla S&P 500 ETF and returns for both the S&P 500 Index and the BuyWrite Index. Two observations emerged from my reivew of the data. (Click on the table to enlarge it.)

From the end of 2007 through September 5, 2012 the S&P 500 was marginally better than flat – returning just over 1% annually on a total return basis. This is the kind of market – say proponents – where covered call strategies shine. And while the BuyWrite Index (BXM) outperformed the plain vanilla (and option-free) S&P 500, its excess return was small. But when looking at the ‘investable’ versions of the two indexes – SPY vs. PBP and BWV – I find that the plain vanilla SPY outpaced both covered call funds. I suspect that this demonstrates the significant costs of executing a covered-call strategy.

Again supporters will point to the substantially lower declines during the last bear market – shown in the table as ‘Biggest Drop’ – as a significant investor benefit. And they’re correct. But risk in the eyes of most investors is a function of both the magnitude of losses and the time spent recovering from losses. Accordingly, it’s difficult to argue that the BuyWrite Index is categorically ‘lower risk’ when investors spend materially more time under water waiting to recover.

Another reason why some of these funds haven’t fully delivered on their promise is that they have a policy of always writing option contracts against their stocks. And there are times – like in late 2008 – when the upside potential is so huge (uncertain as it may be) that it’s really best to stop writing options to have a chance to stocks’ upside potential. This argues for a flexible policy and active management; but the first example above proves this isn’t always the answer.

While it’s worth monitoring how ‘live’ covered call funds perform, the above data confirms my initial view. The lesson is that there are no sure things or free lunches in the world of investing – a lesson that investors have unfortunately been taught many times.