A balanced portfolio’s expected returns

By Dan Hallett, CFA, CFP on June 11th, 2012

I recently provided the Globe & Mail’s Rob Carrick with my long-term expectations for investment returns and inflation over the next decade. With the exception of a couple of outliers – one bull, one bear – I admit to being surprised by the convergence of the dozen estimates. I thought it worthwhile to provide a bit more context to the summary featured in the article and to past return projections.

Return Expectations

Rob Carrick asked what we can expect from a hypothetical portfolio of 60% stocks and 40% bonds in the next decade. My estimate came in at 6.5% annually – with a worst case of 2% and best case return of 8% per year. Here are some important assumptions built into these figures:

- All estimates are based on a simple formula that is driven entirely by asset class fundamentals. When stocks trade at high prices relative to earnings, we’ll expect lower future returns – and vice versa.

- My estimate was based on our firm’s Growth With Income portfolio model, which has the same broad 60/40 asset mix. But this model contains a 40% allocation to global stocks and just 20% to Canadian stocks.

- I assumed that the price that investors are willing to pay for a dollar of earnings (i.e. P/E multiple) will be about the same in 2022 as it is today. Such assumptions are tricky. And as my colleague, Dr. Norm Rothery, recently argued, today’s low interest rates don’t necessarily support a higher multiple. If you’re more bearish and assume that the P/E will fall by 15% to 20% in the coming decade, the portfolio return falls from 6.5% to 5.7% annually.

- I assumed that long-term real earnings growth would be 1% annually, which is 1/3rd lower than the long-term average of 1.5% (to reflect the strong growth in recent years and the fact that deleveraging will moderate future growth).

Future Inflation

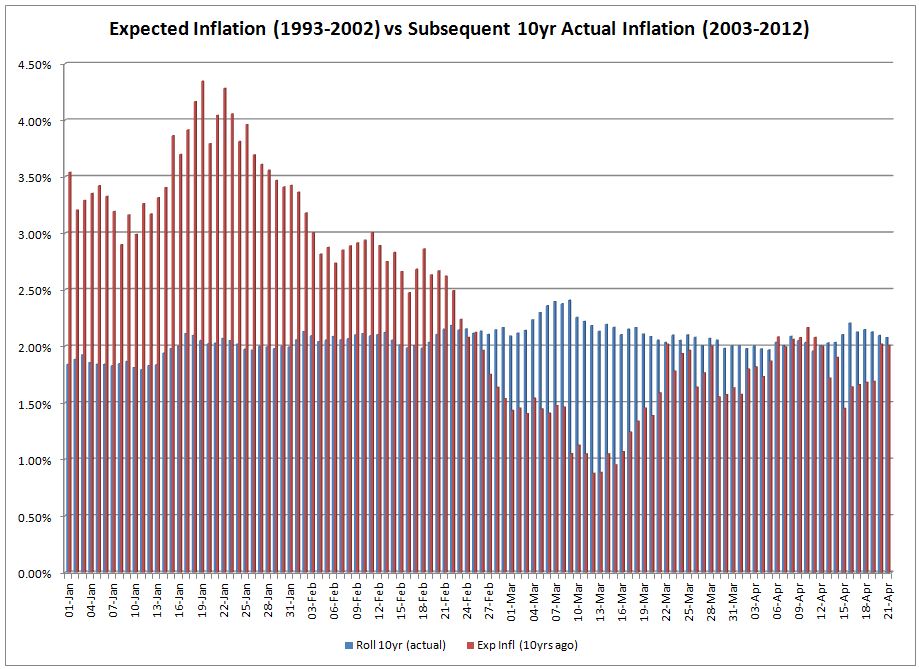

Since I have no particular expertise in this context, I simply looked to what level of inflation is embedded into the prices of North American bond markets. More specifically, inflation expectations can be inferred from the yield differences between Real Return Bonds and traditional long Canada bonds.

While this is as a good an estimate as any, it also hasn’t been terribly accurate. The chart below shows how the inflation rate embedded into Canadian bond prices (i.e. inferring inflation from long Canada bonds and Real Return Bonds) at a point in time compares with actual inflation over the subsequent decade.

It’s worth noting, however, that bond prices a decade ago implied inflation of 2% annually – which is almost exactly what we’ve seen over the past ten years. Still, the overall record doesn’t instill the most confidence. Still, I would still rely more on bond prices than my own forecasting abilities when it comes to something like inflation.

Past Projections

Neither I nor our firm makes a habit of financial market forecasting. But we tend to do so when markets appear to be at extremes (or when asked by journalists we like and respect). The last time I stepped out on a limb was in late 2008 and early 2009. I made my strongest case to buy riskier assets in a November 20, 2008 presentation to a small group of financial advisors and well-heeled investors.

Those were in the darkest days of the 2008-09 financial crisis. But the more time I spent looking at fundamentals – and less time watching the 24/7 business news – the more I was convinced that buying stocks and high yield bonds would pay huge rewards for investors within five years. (The rewards, it turned out, came more quickly and more furiously.)

Prior to that was a presentation I made to financial advisors on September 8, 2001 where I laid out a case for modest stock returns in the decade ahead due to high valuations. It was all fundamentally-driven using a very similar method used for my recent calculations.

Investor Returns

Retail investors have been challenged over the past 10-15 years. Over the past 32 years, the balanced portfolio described above has pumped out 10% per year in returns. But that figure and my 6.5% figure are market-based estimates. In other words, both figures are before incorporating the impact of factors that can enhance (i.e. added value from active management) or erode returns (i.e. fees, inflation, taxes, behavioural gap and value detracted from active management).

Accordingly, it’s likely that ultimate investor returns will fall short of this high level estimate. So it’s important to take any action possible to tilt the odds in investors’ favour.